We expect inflation to have an asymmetric impact - a non-event if the expected downtrend evolves, but any spikes are likely to negatively impact both stocks and bonds. Is there a catalyst for an inflation spike? There are two possible ones in our view - both with a lagged impact. Just as the Fed was late in the tightening cycle, a premature easing is one catalyst with Oil prices being the other. Although it’s early to call for an inflation resurgence, and we remain positive on growth equities, oil prices can be the cliched canary.

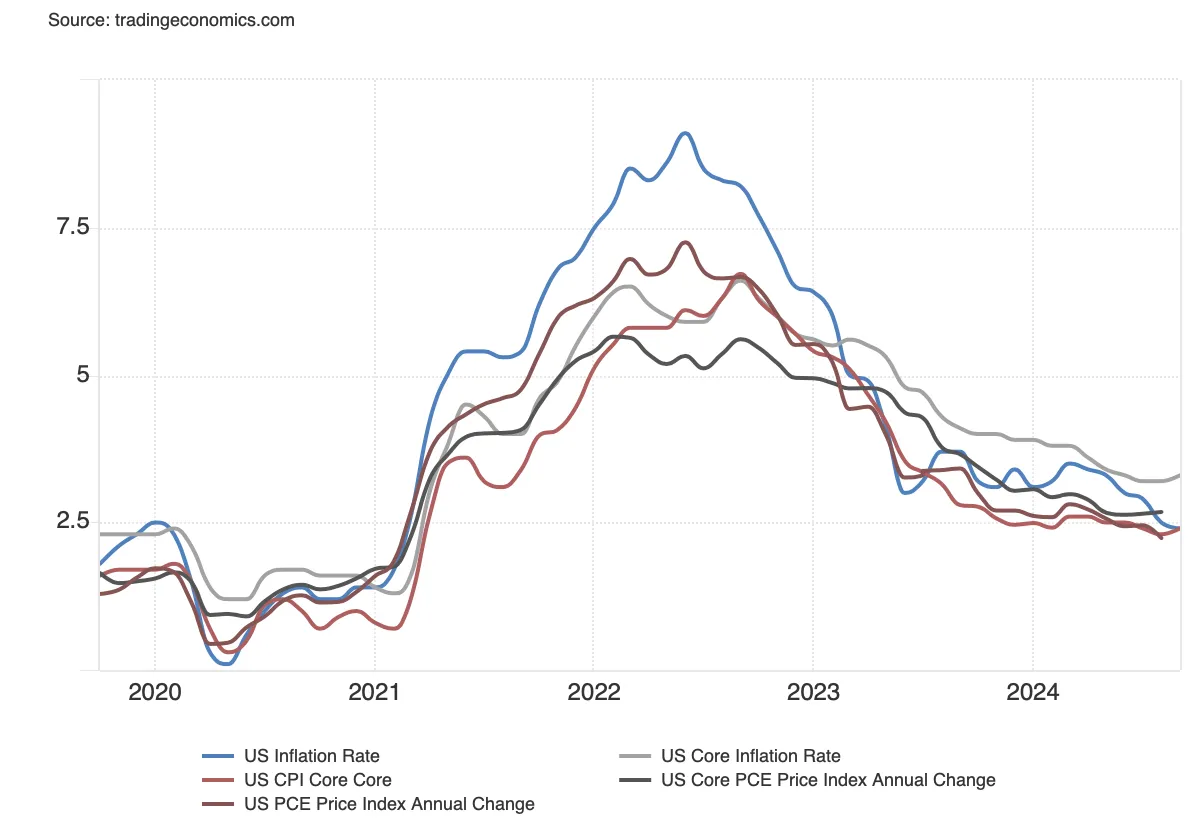

- All measures of inflation move in tandem - Even volatile (food and energy) elements have a pass-through impact on core inflation.

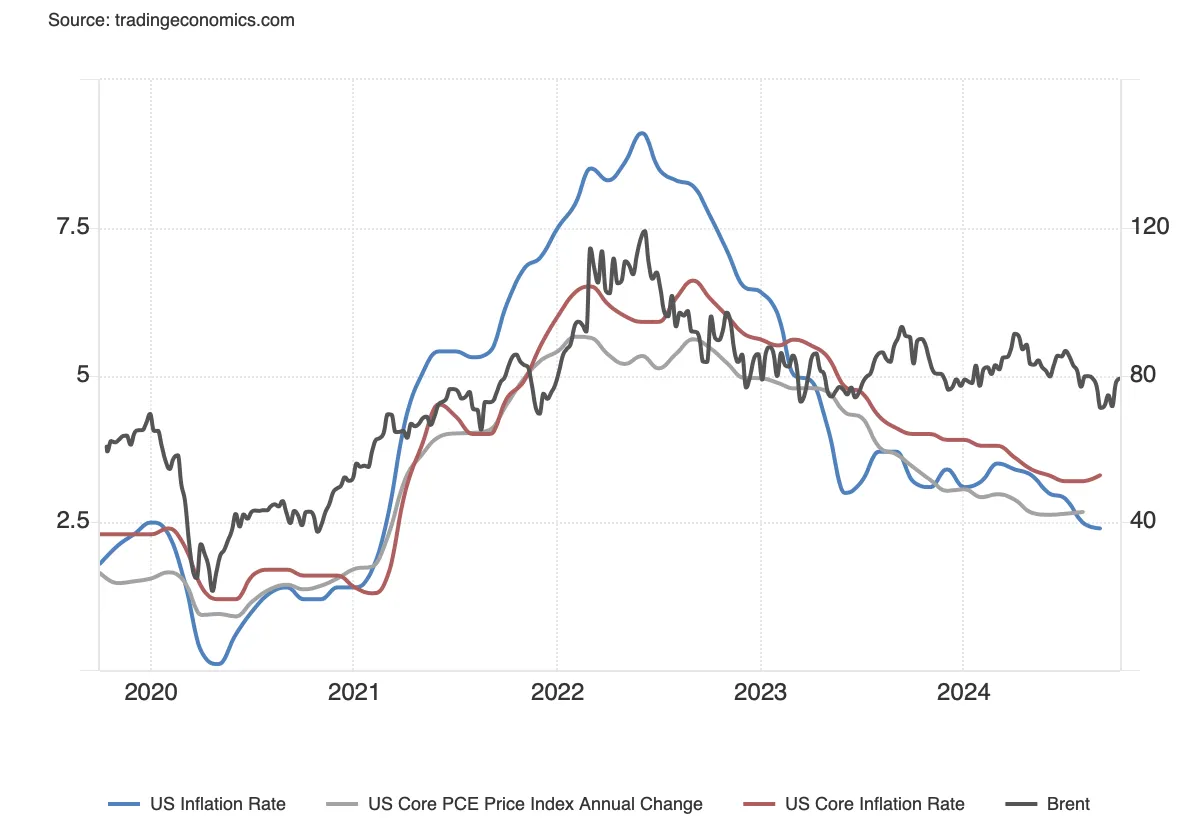

- Oil prices have a clear impact on headline inflation and a sustained trend also on core measures of inflation.

- A sustained rising trend in oil prices, impact risk assets, both stocks and bonds, negatively.

- Should We Worry -NOT YET - Despite a 15-18% rally off the lows, we still don't see the trend as a sustained one - neither on price action, nor on macro data. As such, while less of a concern today, oil price focus becomes paramount.

Positioning

- We remain positive on US growth equities. 3Q earnings season likely to beat a conservative consensus.

- We remain positive on China - tech, domestic consumption and exporters (especially EV makers).

- Both gold and bonds are expected to stall in the near-term. However, gold likely to outperform bonds. For bonds, we have paused on extending duration.

- India, a long-term positive, is likely to see absolute and relative (especially to China) weakness, lacking near term catalysts and the burden of elevated earnings expectations.

Inflation - Core, Headline and PCE

Much attention is focused on core inflation (excluding volatile energy and food) and the FED's preferred PCE. However, trends in all three measures remain aligned - and this is critical. Even though there are volatile elements in headline inflation, the fact is, these do feed into core measures - some directly and some through second order effects. Besides, energy and food prices do impact consumption and hence economic growth.

...from the FED Website (link here) "We find that oil price pass-through to inflation is both economically and statistically significant, and that it occurs both directly and through second-round effects".

..."Including the effect on the energy CPI, a 10 percent increase in the price of oil raises headline CPI by almost 0.4 percent in total."

The Role of Oil Prices

A sustained move in oil prices has a much larger impact on equities and bonds than would appear on the surface. Perhaps markets are quicker to recognize the impact of oil prices on core inflation as well as broad economic growth. We do note however that it needs to be a sustained rise in oil prices to have the adverse impact on stocks and bonds since there is a lag between the feed through into core inflation and economic growth.

- While not necessarily ascribing causality, oil prices are closely correlated with all measures of inflation.

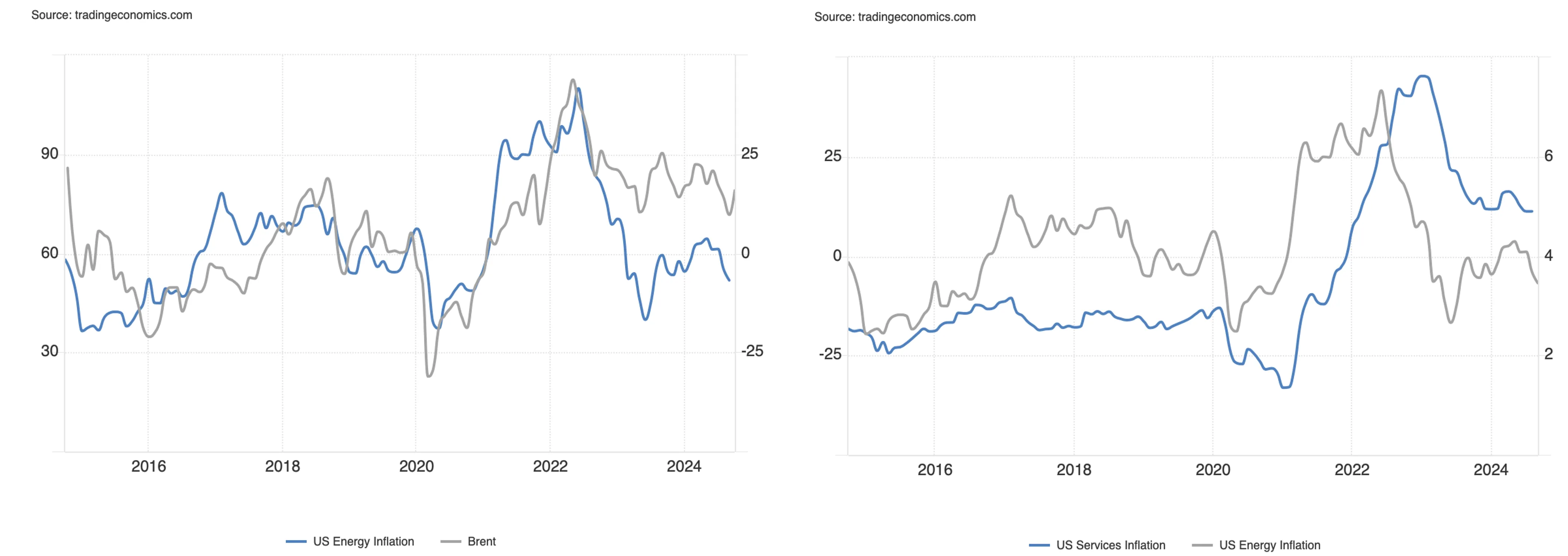

- While energy inflation is closely linked to oil prices, even services inflation (65% of CPI) and energy inflation are closely linked. Within services inflation, c8%pts relate to motor fuel and fuel/utilities in housing.

- 10 year treasury yields closely track oil prices.

Are Oil Prices Going Up? Should We Worry?

- Are Oil Prices Going Up - YES

- Is This a Sustained Trend - NOT YET

- Should We Worry - NOT YET

While oil prices have risen 15-18% off lows, predominantly led by geopolitical tensions in the Middle East, price action has been choppy enough for this not to be classified as a sustained upward trend. For that to materialize, we will probably need to see a sustained rebound in economic growth, especially in China. There just isn't enough evidence, either in macro data or price action, to cause immediate concern.

While not a concern on a visible horizon, this can change rapidly - so oil price monitoring becomes super important.

- Oil Price Technicals - Recent rally breaks through downtrend-line (in force since Jul-Aug'24), supported by positive momentum (RSI and z-score) and positive MACD positioning. Overhead resistance in the $82 area is significant. A sustained breakout above $82 risks moves up.

All investments carry risk, for more important information please read this disclaimer.

.png)

%20(13).png)