Up 23% + in the last 8 days the Hang Seng Index has returned almost all of what it managed to over the past 10 years (31.4%).The combination of fiscal and monetary policy announced by China last week has provided a much-needed boost to the Chinese equity markets, which have underperformed other global indices by a significant extent over the last 10-years.

Will this rally in Chinese securities continue?

The structural issues (highly leveraged balance sheets; youth unemployment etc.) that have plagued the Chinese economy won’t be solved overnight, but what has been seen time and again is that equity markets tend to be forward looking and move 6-9 months ahead of the underlying fundamentals. Based on this, we believe that the recent momentum, positive flow into the Chinese markets should not be ignored and provide an opportunity to build up positions in high quality bottom-up opportunities, which continue to trade at dirt-cheap valuations even after the sharp move seen over the past 2-weeks.

How to position?

- Index / broad market ETFs tend to have all category of businesses, and the lower rung businesses (from a quality perspective) tend to be first when it comes to profit taking and stalling out after a large broad-based move in the indexes and hence such ETFs tend to deliver diffused performance. However, we believe that these can be a viable alternative for investors looking to gain exposure to a revival in broad based investor sentiment surrounding Chinese equities.

We’re also bullish on the following themes where we see the highest chance of sustained earnings growth and re-rating of valuation multiples which have not differed by much, based on quality (as they usually/must do) across Chinese stocks during this period of sluggish growth and policy uncertainty :-

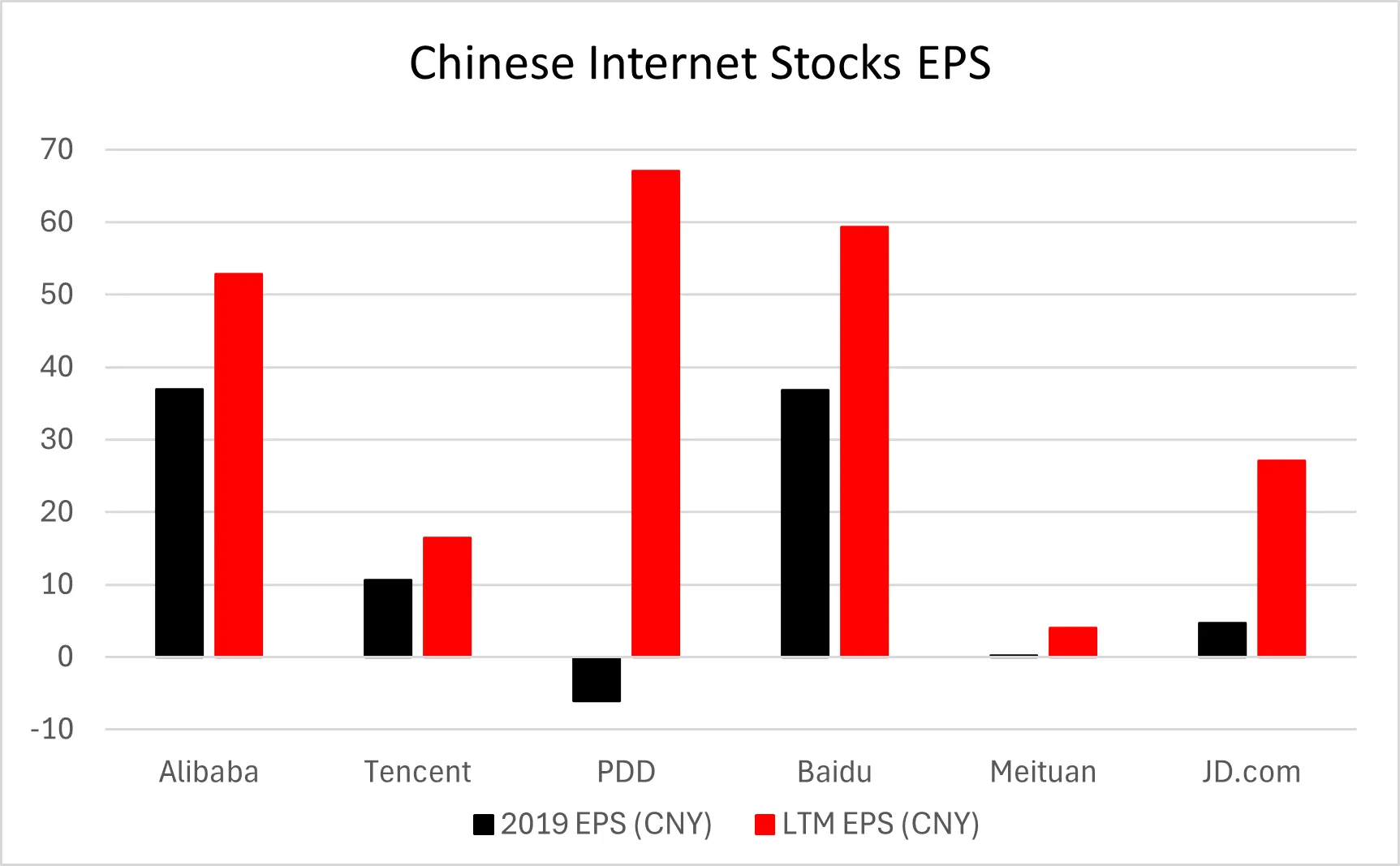

- Tech / internet stocks have grappled with a whole host of issues, led by the crackdown on internet companies by the Government, for over-earning. While these companies are unlikely to see a return to peak profitability (in terms of the return on investment that they were earning), we are certain that they will manage to grow their earnings at a reasonable pace over the next decade, something that they managed to do even during the post pandemic period. Yet, these stocks have corrected significantly from their highs established back in 2021 (down on an average 40% from the peak), which essentially signifies a significant compression in their P/E ratios, which for some select high quality businesses makes absolutely no sense to us and presents meaningful room for a re-rating to happen.

- Domestic consumption-oriented stocks have had a tough run over the past few years as China has grappled with an autonomous increase in domestic savings and a lack of willingness to borrow money given the uncertainty surrounding the economy and government policy. The set of monetary and fiscal measures announced together, are specifically targeted towards remedying this situation and this should help companies serving the domestic consumers get a kickstart in terms of earnings recovering from the lows (which have suffered significantly ever since Covid). Further, these stocks trade at depressed valuation multiples which are quite a bit below what they have historically traded for.

.webp)

- Chinese automobile businesses have taken over the world’s production of cars over the past few years and we believe that their domination is set to increase over the coming decade as once again when it comes to manufacturing, no one seems to be able to match China on pricing. Additionally, we would also like to note that the Teslas of the world are not too far ahead when it comes to the technological aspect of modern-day cars (ADAS, battery technology, car efficiency and performance). Further, we feel that the European automobile manufacturing business is pretty much broken, given that it just does not work without the cheap energy that they used to source from Russia. Just in the last week we have seen Stellantis miss its numbers; Volkswagen issue its second profit warning in 3-months and Aston Martin issue a profit warning as well. Much of this loss of market share that the European auto-manufacturers are facing is due to Chinese companies selling cars that are much cheaper and arguably of a higher quality. While the sanctions placed by EU definitely have an impact, we doubt whether they’ll be able to defend the interests of the domestic manufacturers which have fallen off quite significantly on the quality and pricing front.

.webp)

All investments carry risk, for more important information please read this disclaimer.

%20(13).png)

%20(11).png)

%20(9).png)

.png)