Moderna's disappointing revenue guidance for 2025 extended the stock's drawdown which has now reached a whopping 94%, from the peak established back in 2021 at the height of the covid-19 pandemic.

We see this correction in Moderna's stock price to be significantly overdone at this juncture, given that the entire business is selling for $13.26 Billion (1.1x book value), while having a net cash position of $5.5 Billion and a total cash and investments of $9.2 Billion. Further, one must add to this their significant late stage pipeline, which is made up of multiple compounds that are likely to be commercialized in the coming 3 years and many of them will cater to multi-billion $ markets.

Based on the above, we believe that the market is significantly discounting the company's ability to generate meaningful and sustainable earnings, cashflow over the next 5-10 years -something that a long term investor, capable of weathering a significant amount of stock price volatility can take advantage of.

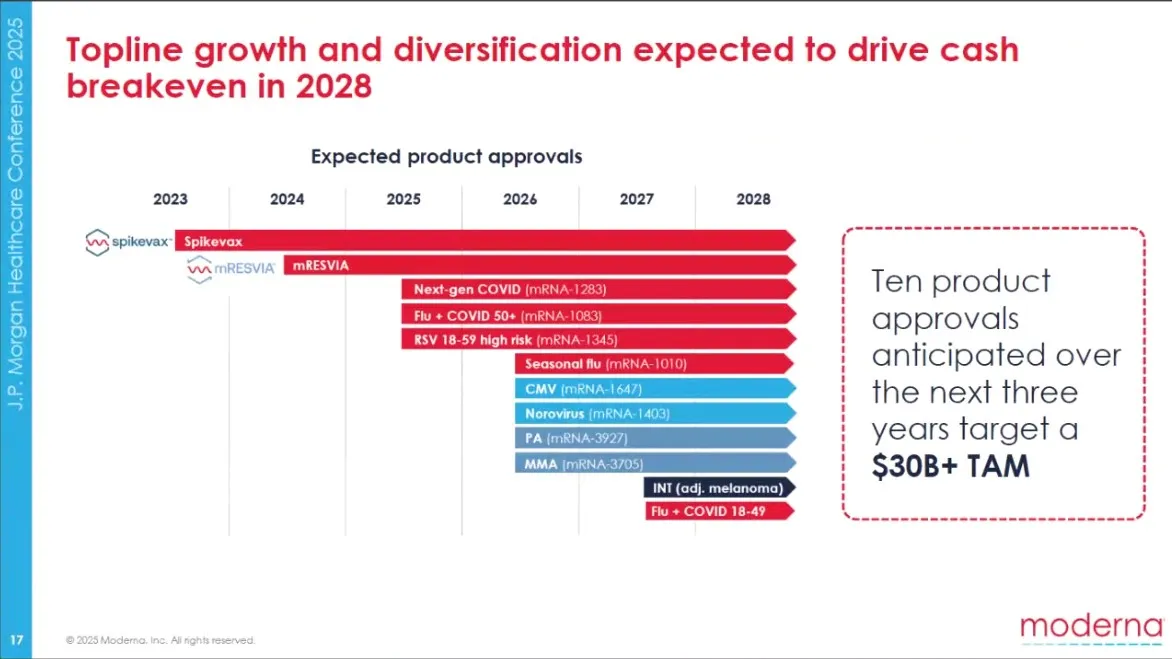

Key assets in the Pipeline and their expected date of commercialization :-

- Respiratory Syncytial Virus (RSV) Vaccine: The company has already received approval for the vaccine in the senior adults segment and is expected to receive approval for high risk individuals in the 18-59 years age bracket this year.

- Influenza Vaccine: The influenza vaccine has a huge TAM and will be further developed to be merged with Covid-19 and other respiratory diseases (RSV) and therefore be administered in the form of a combo vaccine, which provides them with a massive competitive advantage. Additionally, we believe that Pfizer’s combo vaccine (Influenza + Covid-19) failure announced last year, provides further confidence to us that Moderna will be the leading player in the Influenza vaccine market.

We expect approval for the standalone Influenza vaccine in H1 2025 and the combo vaccine (Influenza + Covid-19) to be approved in H2 2025.

Further, they also plan to bring a more advanced combo vaccine to the market, which packages 3 respiratory vaccinations (Influenza + Covid-19 + RSV) in to one shot.

- Individualized Neoantigen Therapy (Personalized cancer vaccine) being developed in partnership with Merck's Keytruda: The treatment has been granted break-through designation and is currently in phase 3 testing for multiple cancer indications, such as melanoma & non small cell lung cancer. We expect approval for the treatment of melanoma to come in 2027 and other indications coming through soon after.

Further, the results for this therapy have been positive across multiple forms of cancer and the company has steadily been adding additional indications to the pipeline (bladder cancer; early & late stage solid tumors etc.) and we believe that this is the most promising asset in the company's pipeline and could end up raking in $2-3 Billion in revenues every year (if not more).

- Rare disease therapies such as Propionic acidemia & Methylmalonic acidemia: While the addressable market for these treatments is small, they will carry rare disease pricing and add meaningfully to the profitability of the company. Both of these treatments are likely to be approved in 2026.

- Cytomegalovirus (CMV) Vaccine: Expected to be approved in 2026.

- Norovirus Vaccine: Expected to be approved in 2026.

Overall, we believe that the market's short-term hyper efficiency, is causing it to take a rather myopic view of Moderna as a company and what their mRNA platform is likely to deliver in the upcoming 3-5 years. Current valuations of slightly more than 1 time book value essentially represents the company's large late-stage pipeline being given away for almost no cost and many other early stage compounds which have significant potential, to be completely ignored.

We expect the company to post a topline of approximately $6-8 Billion and breakeven by 2028, post which the ramp up in sales of commercialized compounds and additional assets being commercialized will translate into a significant amount of economic profits, at which point the stock is bound to appreciate.

However, we would like to note that the stock is likely to remain significantly volatile during this period, with the Street continuing to fixate on what the company is doing in 2025 and 2026, largely discounting the value that is there to be unlocked in its pipeline (till it is actually unlocked). The company's ability to execute on its pipeline is another key monitorable in our opinion and we expect bouts of volatility to be common around pivotal data read-outs and PDUFA dates.

All investments carry risk, for more important information please read this disclaimer.

%20(15).png)

.png)